… What Residential Mortgage Lenders Disallow Second Mortgagees

When borrowers or even brokers ask:

“Which lenders don’t allow second mortgages?”

They’re asking the wrong question.

Because in residential lending, the reality is this:

It’s not just the lender—it’s the loan type, the insurance status, and the mortgage contract that determine whether a second mortgage is allowed.

And in many cases, second mortgages are not just discouraged…

They are explicitly prohibited.

Allow me to get into it:

Insured Mortgages: Absolute “No”

First Mortgage Contract Restrictions (The Real Gatekeeper)

Major Banks (Schedule A Lenders): Practical “No”

“Silent Seconds”: Completely Illegal

HELOC and Collateral Charge Structures

When Consent Is Required (And Often Denied)

The Underlying Reason: Risk Hierarchy

When Lenders Are Most Likely to Say “No”

The Exception: When Second Mortgages Are Allowed

The Core Rule

Before we even get into lender categories, understand this:

A second mortgage is not automatically allowed just because you have equity.

Most first mortgages include legal clauses that:

- Restrict additional financing

- Require lender consent

- Or prohibit secondary encumbrances entirely

If you ignore that:

- You can trigger default on your first mortgage

- The lender can demand full repayment

This isn’t theory—this is how the contracts are written.

FSRA Enforcement

The Financial Services Regulatory Authority of Ontario (FSRA) reported in a recent Enforcement Annual Report, cited enforcement action outcomes for Forest City Funding Inc. (FCF) and William Handsaeme. During a supervisory examination, FSRA determined that FCF knowingly assisted borrowers in obtaining a second mortgage that contravened the terms and conditions of the first mortgage FSRA also determined that second mortgages were being used to pay back supposedly “gifted” down payments, contrary to the terms of the first mortgage commitments. The issue was communicated to FCF, but was not resolved when a follow-up examination was conducted.

In another enforcement action outcome, Jaswinder Dhanoa was a mortgage agent who submitted fraudulent downpayment and income verification documents to a lender on multiple occasions. Additionally, some properties had second mortgages contrary to the terms of the first mortgage and for amounts consistent with the fraudulent down payment. Ms Dhanoa received fees for these mortgages paid to her personal corporation outside of her authorizing mortgage brokerage. Following a settlement and the expiration of Ms Dhanoa’s licence, FSRA imposed AMPs totalling $52,000, reflecting the entire monetary gain.

Source: www.fsrao.ca

Insured Mortgages: Absolute “No”

This is the clearest category.

If the mortgage is insured:

- High-ratio (less than 20% down)

- Backed by insurers like:

- CMHC

- Sagen

- Canada Guaranty

Second mortgages are effectively not allowed

Why?

Because:

- The insurer must control risk completely

- The first mortgage must remain the sole secured position

- Additional registered debt increases default exposure

Even though second mortgages exist as a concept, insured structures are built to prevent layered risk.

First Mortgage Contract Restrictions (The Real Gatekeeper)

This is where most deals get blocked.

Even if a lender “technically allows” second mortgages, the mortgage agreement may not.

Most residential mortgage contracts include:

- “No further encumbrance” clauses

- Requirements for lender approval

- Restrictions on additional secured borrowing

Which means:

You must get consent from the first lender before adding a second mortgage.

If you don’t:

- It can be considered a breach

- It can trigger default

- The lender can “call” the mortgage

That’s not a grey area—it’s black and white.

Major Banks (Schedule A Lenders): Practical “No”

Let’s talk about behaviour—not marketing.

The major banks:

- RBC

- TD

- BMO

- Scotiabank

- CIBC

Will often say:

“Second mortgages may be allowed with consent”

But in practice:

They rarely approve them

Why?

Because from the bank’s perspective:

- They lose control over collateral

- Combined leverage increases risk

- Another lender is now behind them on title

And remember:

The first mortgage lender gets paid first in a default scenario.

Banks want to keep it that way—with no complications.

“Silent Seconds”: Completely Illegal

This is critical.

A silent second mortgage (undisclosed secondary financing): Is illegal in Canada

Why?

- The first lender must be aware of all secured debt

- Undisclosed borrowing distorts qualification

- It creates systemic risk

This is not just a policy issue—it’s a legal one.

HELOC and Collateral Charge Structures

This is where things get more nuanced.

Some lenders structure mortgages as:

- Collateral charges

- Readvanceable products (e.g., mortgage + HELOC)

In these cases:

The lender often locks down the title

Meaning:

- No additional lenders can register behind them

- They control all future borrowing

Even if it’s not explicitly stated, the structure itself:

Effectively disallows second mortgages

When Consent Is Required (And Often Denied)

Even in cases where second mortgages are possible:

You will often need:

- Written consent from the first lender

- Full disclosure of terms

- Approval of the new structure

And here’s the reality:

Consent is frequently denied

Because the lender is asking:

- Does this increase default risk?

- Does this weaken our position?

If the answer is yes:

The deal stops there

The Underlying Reason: Risk Hierarchy

Everything comes back to one concept:

Priority of repayment

- First mortgage = paid first

- Second mortgage = paid second

If the property is sold under distress:

- The first lender is protected

- The second lender takes the loss

That’s why second mortgages are considered higher risk and priced accordingly. (Canada)

And that’s why first lenders are extremely protective of their position.

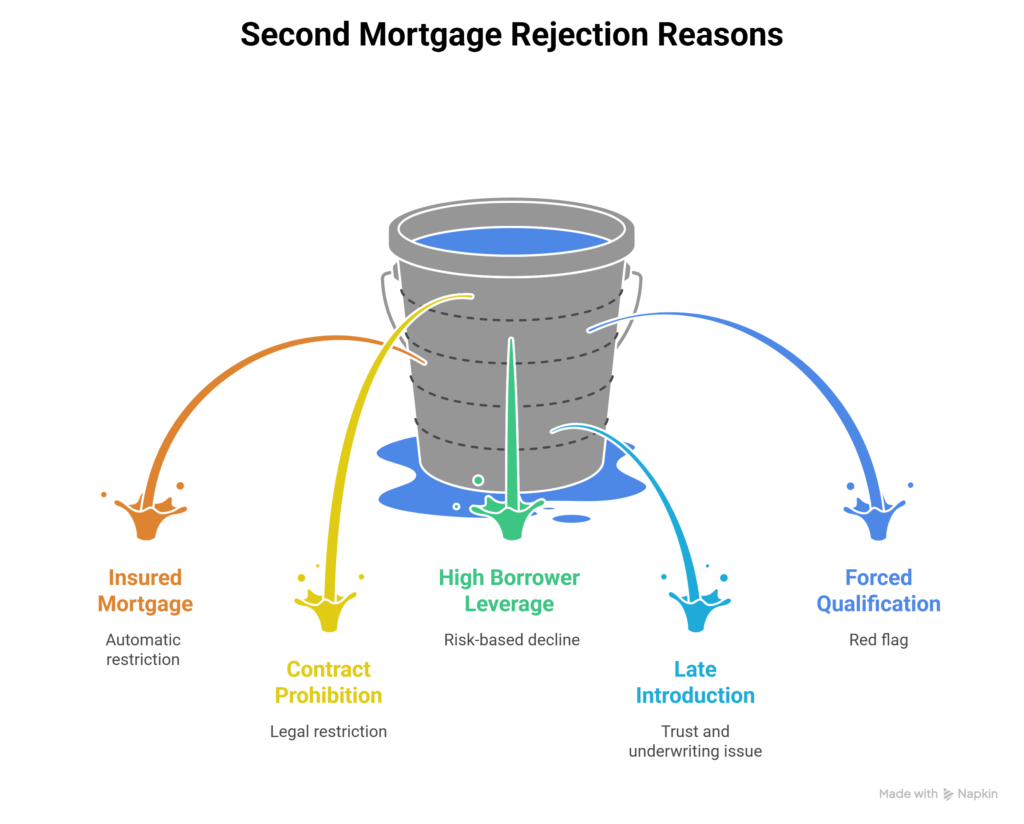

When Lenders Are Most Likely to Say “No”

Across all residential lending, second mortgages are typically disallowed when:

1. The mortgage is insured

→ Automatic restriction

2. The mortgage contract prohibits it

→ Legal restriction

3. The borrower is already highly leveraged

→ Risk-based decline

4. The second mortgage is introduced late

→ Trust and underwriting issue

5. The structure appears to “force qualification”

→ Red flag

The Exception: When Second Mortgages Are Allowed

To be clear, they are not always disallowed.

They are possible when:

- The first lender consents

- The borrower has strong equity

- Combined LTV remains within acceptable limits (often ≤80%)

- The structure is disclosed upfront

- The purpose makes sense

But notice the pattern:

These are controlled, structured scenarios—not default options

The Real Takeaway

The industry often frames this as:

“Which lenders allow second mortgages?”

But the truth is:

Most residential lenders disallow second mortgages by default—unless the structure fits their risk model perfectly.

Allen’s Final Thoughts

Second mortgages are not just about access to equity.

They are about:

- Legal structure

- Lender priority

- Risk control

And in residential lending, the first mortgage lender:

Always comes first—by design, by contract, and by enforcement.