… Why We Fear What We Asked For

You’ve probably heard it for years: “We need more homes, so prices will come down and things will finally be affordable again!”

Sounds logical, right? Build more houses, prices drop, everyone wins. But here’s the kicker—prices are now dropping in many markets, and instead of celebration, there’s panic. Builders are pausing projects, policymakers are scrambling, realtors have no business, and homeowners are worrying about their equity. Who wants to buy a house for a million dollars today that will be worth $900,000 this time next yere?

Why do we panic when we finally get what we said we wanted? Let me break down what’s really going on and what it means for you, whether you’re a realtor guiding clients or a homeowner trying to navigate this market.

Allow me to Cover

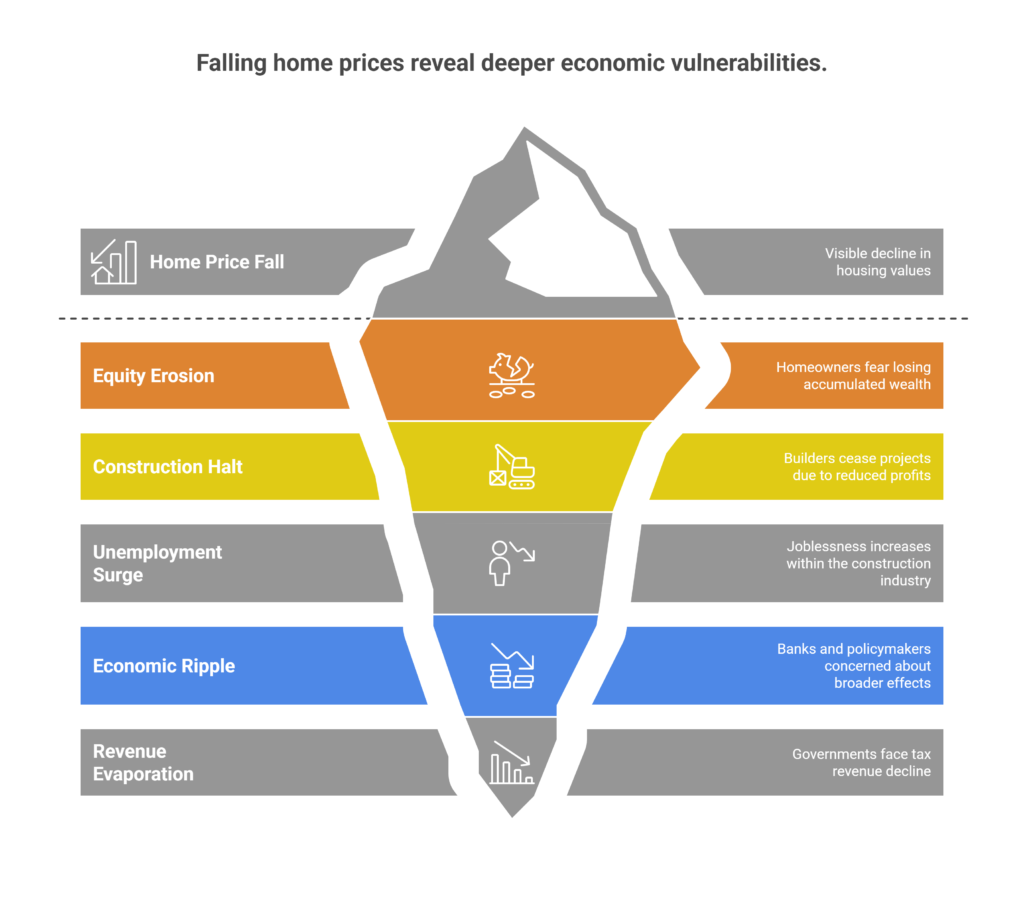

Why Falling Prices Cause Panic Instead of Relief

The Myth of Endless Building Solving Everything

How Realtors and Buyers Can Put This Knowledge to Work

Why Falling Prices Cause Panic Instead of Relief

Housing is different from almost anything else we buy. When the price of TVs drops, no one freaks out; we celebrate. But with homes, we treat them not just as shelter but as one of our biggest investments.

When home prices fall:

- Homeowners worry about losing equity they’ve built up over decades.

- Builders stop building because their profit margins shrink.

- Unemployment in the sector sky rockets.

- Banks and policymakers worry about economic ripples—because so much of our economy runs on real estate.

- Governments panic because tax revenue evaporates.

So while falling prices should improve affordability, they actually disrupt an entire system that was built on rising home values.

The Myth of Endless Building Solving Everything

For years, we’ve been told, “Just build more homes and prices will fall.” In theory, yes—more supply can help affordability. But what happens when those prices actually fall? Many builders stop building altogether.

Why? Because housing isn’t like making widgets in a factory. A builder who bought land at peak prices isn’t going to happily sell at a loss. And if prices dip by 20% or 30%, as we’ve seen in Ontario, it becomes uneconomical to keep building at the same pace.

This isn’t a sign that anyone is evil or broken; it’s how the system is designed. We built our housing model on asset inflation, not true affordability—and now we’re seeing what happens when the system’s assumptions get tested.

A Story That Brings It Home

Meet Julie and Peter, a couple in their early 40s who bought their first home in 2021 at the top of the market. They paid $1,250,000 for a suburban detached home, believing prices would keep rising. Fast-forward to 2025: similar homes are selling for $800,000. 85% of people who bought homes in the last 5 years are now underwater… and that number will grow.

Peter called me last month, panicked: “We’ve lost $450,000 on paper—should we sell before it drops more?”

After talking through their finances, we realized they weren’t in trouble. Their mortgage was affordable, and they still loved the home. But the psychological hit of seeing their home “lose value” made them feel like they failed. They did lose real equity. Their net worth is lower today.

The reality? If they planned to live there long-term, nothing had changed except a number on paper (pre-supposing they don’t plan to refinance, do an equity take out, or get a second mortgage) But their fear? That’s what falling prices do—they shake confidence, even when the fundamentals are solid.

The value of their home as dropped, but their mortgage and their property taxes haven’t.

I thought property taxes were based on property value assessment. If property values are lower, shouldn’t property taxes be lower?…. just a thought

How Realtors and Buyers Can Put This Knowledge to Work

For realtors:

- Reframe the conversation. Remind sellers and buyers that price cycles happen and that most homeowners are in it for the long haul.

- Focus on needs, not speculation. Encourage buyers to choose homes they can afford and plan to live in, not just invest in.

- Help nervous sellers. Some homeowners panic-sell in declining markets, which can hurt them. Educating clients on long-term value can prevent rushed decisions.

For buyers:

- See opportunity, not fear. If prices are down, you may finally get the home you want with a manageable mortgage.

- Think long-term. You’re buying a home, not a day-trading stock. If you can afford it, short-term price swings don’t matter as much.

Allen’s Final Thoughts

The panic over falling home prices shows how emotionally tied we are to housing as an investment instead of just a home. For decades, we built expectations—and policies—on endless growth. But housing markets are cyclical. Prices will rise and fall, and that’s normal.

Instead of panic, this can be a time for opportunity. It’s a chance to buy smart, think long-term, and focus on real-life needs instead of short-term price charts.

How I Can Help as Your Mortgage Agent

This is where I come in. My job is to help you navigate these shifts with confidence:

- If you’re buying, I can help you secure a mortgage strategy that works even in uncertain times.

- If you’re nervous about your payments, I can explore refinancing or restructuring options to protect your cash flow.

- If you’re an investor or realtor, I can help you understand financing trends so you can advise clients with confidence.

Whether home prices are rising or falling, your home should support your life—not stress you out. Let’s talk about strategies that keep you secure and moving forward, no matter where the market goes.