In Canada, there are about 10 different kinds of lenders, offering prime, alternative, and subprime mortgages that are insured, uninsured, and insurable while also being conventional or collateral. There are literally thousands of different mortgage products on the market, coming to the market and disappearing from the market all the time. So which do you choose?

Mortgages are in some ways a lot like pharmaceuticals. A drug that is good for one person is bad for another. So too is it with mortgages and financial products in general. This is why it is important to work with a license professional to discover the mortgage that is best for you.

For Canadian homeowners seeking a flexible mortgage structure, Scotiabank’s Scotia Total Equity Plan (STEP) offers a dynamic financial solution. Unlike a traditional mortgage, STEP allows borrowers to combine multiple loan components under a single plan, integrating fixed-rate mortgages, variable-rate mortgages, and a home equity line of credit (HELOC). This structure makes it an appealing choice for those who need a mortgage that adapts to their financial situation over time.

However, not every borrower will benefit from the Scotia STEP mortgage. In this guide, I’ll explore its features, who it suits best, and who might be better off with a simpler mortgage solution.

Understanding the Scotia Total Equity Plan (STEP)

Who Benefits Most from the Scotia STEP Mortgage?

Who Should Avoid the Scotia STEP Mortgage?

Example Scenario: How a Family Uses Scotia STEP

Understanding the Scotia Total Equity Plan (STEP)

Scotiabank STEP is designed as a customizable borrowing solution that allows homeowners to manage their mortgage and home equity more effectively. This product provides the ability to split mortgage borrowing into different portions, including:

- Fixed-rate mortgage portions, which provide predictable payments over a set term.

- Variable-rate mortgage portions, which allow borrowers to benefit from lower rates when the market fluctuates.

- Home Equity Line of Credit (HELOC), which offers revolving credit that increases as the mortgage principal is paid down.

- Additional borrowing accounts, which can be used for personal loans or investment purposes.

The defining feature of STEP is its readvanceability—as the borrower makes payments toward the mortgage, the HELOC’s available credit increases automatically. This makes it particularly attractive for homeowners who want continuous access to home equity without having to reapply for credit.

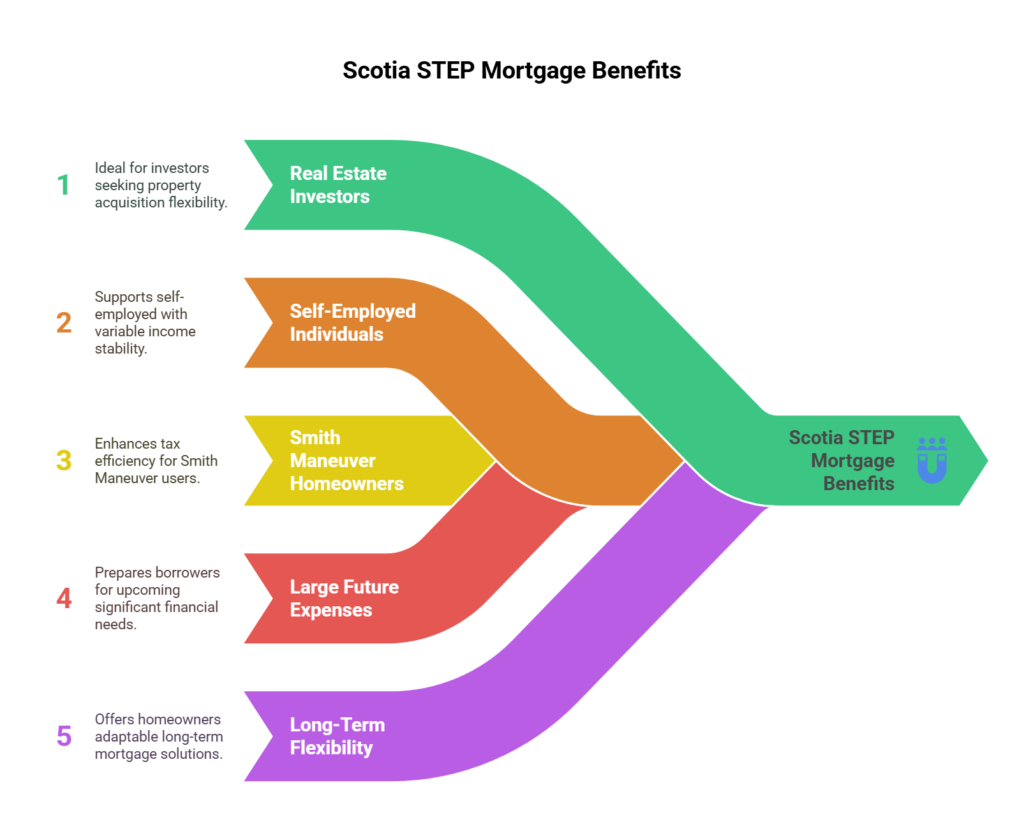

Who Benefits Most from the Scotia STEP Mortgage?

Scotia STEP is an excellent choice for borrowers with complex financial needs or those who wish to take a strategic approach to their mortgage and investments. The following groups stand to benefit the most:

- Real Estate Investors

- Self-Employed Individuals and Commission-Based Earners

- Homeowners Implementing the Smith Maneuver

- Borrowers Planning for Large Future Expenses

- Homeowners Seeking Long-Term Flexibility

Real Estate Investors

Real estate investors often require flexible financing solutions, and Scotia STEP allows them to separate their mortgage into different segments for multiple properties. Additionally, the HELOC portion enables investors to access equity for down payments on future investments without the need for refinancing. Interest on the HELOC may also be tax-deductible if used for income-generating investments.

Self-Employed Individuals and Commission-Based Earners

For those with variable income, such as realtors, consultants, and business owners, cash flow management is crucial. The HELOC serves as a financial buffer, helping cover expenses during slower months without requiring new loan applications. Scotia STEP also allows borrowers to segment mortgage components, making it easier to distinguish between business and personal borrowing.

Homeowners Implementing the Smith Maneuver

The Smith Maneuver is a tax-efficient borrowing strategy that converts mortgage debt into tax-deductible investment debt. Because STEP is fully readvanceable, it allows homeowners to access their growing HELOC balance for investment purposes as they pay down their mortgage. This makes it one of the most suitable mortgage products for long-term wealth-building through leveraged investing.

Borrowers Planning for Large Future Expenses

Homeowners who anticipate significant expenses, such as home renovations, RESP contributions, or business investments, will appreciate the easy access to funds through the HELOC portion of STEP. Instead of applying for new loans, they can simply withdraw funds from their HELOC as needed.

Homeowners Seeking Long-Term Flexibility

Some borrowers want the ability to switch between fixed and variable mortgage portions without the hassle of refinancing. Scotia STEP allows for seamless transitions between different loan structures, ensuring the mortgage remains aligned with evolving financial goals.

Who Should Avoid the Scotia STEP Mortgage?

Despite its many advantages, Scotia STEP is not the best option for every borrower. Those who prioritize simplicity or have more straightforward mortgage needs might find it unnecessary. Here are some groups that may not benefit from STEP:

- First-Time Homebuyers with Small Down Payments

- Homeowners Who Prefer a Simple Mortgage Structure

- Borrowers Who Do Not Plan to Use Their Home Equity

- Those Seeking the Lowest Possible Mortgage Rate

First-Time Homebuyers with Small Down Payments

Borrowers putting down less than 20% do not qualify for the HELOC portion of STEP. For these individuals, a traditional fixed or variable mortgage with a lower overall cost may be the better choice.

Homeowners Who Prefer a Simple Mortgage Structure

Some borrowers do not require multiple mortgage components or the flexibility of a HELOC. If the goal is simply to obtain a low, predictable mortgage payment, a traditional mortgage—such as those offered by TD or BMO—may be more appropriate.

Borrowers Who Do Not Plan to Use Their Home Equity

If a homeowner has no intention of borrowing against their home equity, there is little reason to opt for a readvanceable mortgage. A standard mortgage might offer a lower interest rate and simpler repayment structure.

Those Seeking the Lowest Possible Mortgage Rate

Since Scotia STEP includes a HELOC feature, the interest rate on the mortgage portion may be slightly higher than non-readvanceable mortgages. Borrowers who prioritize the lowest possible rate might find better options with other lenders.

Example Scenario: How a Family Uses Scotia STEP

Background: John and Sarah Smith are a married couple with two children. John works as a real estate agent with fluctuating income, while Sarah is a dental hygienist with a stable salary. They recently purchased an $800,000 home with a 20% down payment ($160,000), leaving them with a $640,000 mortgage. Their primary financial goals include maintaining affordable mortgage payments, preparing for their children’s education, and investing in real estate.

How They Structure Their Scotia STEP Mortgage:

| Loan Component | Amount | Rate | Term | Purpose |

| Fixed-Rate Mortgage | $320,000 | 5.19% | 5 Years | Provides stability using Sarah’s income |

| Variable-Rate Mortgage | $160,000 | 5.00% | 5 Years | Adjusts to market conditions based on John’s income |

| HELOC (Interest-Only Payments) | $160,000 | Prime + 0.50% (7.2%) | Open | Used for investments and emergency buffer |

Results:

- Their monthly mortgage payments remain predictable, ensuring stability for their family’s budget.

- John can use the HELOC to cover slower real estate sales periods while keeping the mortgage separate.

- As they pay down the mortgage, their HELOC increases, allowing them to invest in a rental property without refinancing.

Why Scotia STEP Works for Them:

- It provides a balance of stability (fixed) and flexibility (variable + HELOC).

- They can invest while still paying down their home.

- The HELOC serves as an emergency fund without the need for personal loans.

Is Scotia STEP Right for You?

The Scotia Total Equity Plan is a highly flexible mortgage product designed for homeowners who want to manage their mortgage dynamically. It is particularly beneficial for real estate investors, self-employed individuals, and those implementing the Smith Maneuver.

However, for borrowers who prefer a straightforward mortgage or do not plan to use their home equity, a traditional fixed or variable mortgage may be a better fit.

Give me a call if you would like a personalized recommendation to determine if Scotia STEP is right for you.