Did you know 73% of Canadians have some debt? The average household debt is $1.77 for every dollar of disposable income. This shows the need for good debt relief in Canada. A debt management plan is a strong tool to help you manage your finances and work towards being debt-free.

A debt management plan is a way to handle overwhelming debt. It’s a strategy to combine many debts into one easy monthly payment. This plan is made just for you, helping when you’re overwhelmed by bills and creditor calls.

For many Canadians, a debt management plan is a ray of hope. It’s not just about paying off debt; it’s about learning to handle your money better. With expert help and a good plan, you can enjoy lower interest rates, no extra fees, and a clear path to financial freedom.

Understanding Debt Management Plan Basics

Signs You Need Professional Debt Relief

The Role of Credit Counselling in Debt Management

Comparing Debt Management Plan with Other Solutions

Steps to Enroll in a Debt Management Plan

Monthly Payments and Program Duration

Working with Creditors Through Your DMP

Common Mistakes to Avoid During Debt Management

Key Takeaways

- Debt management plans consolidate multiple debts into one payment

- DMPs can lead to reduced interest rates and waived fees

- Professional credit counselling is often part of the DMP process

- A DMP helps you develop better money management skills

- It’s a structured approach to achieving long-term financial stability

Understanding Debt Management Plan Basics

A debt management plan (DMP) is a strong tool for Canadians with financial troubles. It helps you manage your debts and work towards being debt-free.

Key Components of a DMP

DMPs usually have:

- Consolidation of unsecured debts

- Negotiated interest rate reductions

- A single monthly payment

- Structured repayment timeline

DMP Process in Canada

In Canada, DMPs begin with a meeting with a credit counsellor. They look at your finances, make a budget, and talk to creditors for you. You pay one monthly amount to the credit agency, which then pays your creditors.

Benefits for Canadian Consumers

DMPs bring many benefits:

- Simplified debt repayment

- Potential interest rate reductions

- Protection from collection calls

- Improved financial planning skills

Joining a DMP is a big step towards financial stability. It not only manages your debts but also teaches you about financial planning for the future.

Signs You Need Professional Debt Relief

Knowing when you need debt relief is key for your financial health. If you’re battling debt, some signs show it’s time for professional help.

Missing payments often is a big warning sign. Not being able to pay bills on time means your debt is hard to handle. Using credit cards for daily needs like food or fuel also shows financial trouble.

If debt feels too much to handle, it’s time to think about credit counselling. Experts can offer strategies for managing and reducing your debt.

| Warning Sign | What It Means | Action to Take |

|---|---|---|

| Missed payments | Inability to meet financial obligations | Seek debt relief options |

| Using credit for essentials | Living beyond your means | Review budget and spending habits |

| Feeling overwhelmed | Emotional stress from financial strain | Consult a credit counselling service |

Don’t ignore these warning signs. Getting help early through debt relief programs can stop more financial harm. Remember, asking for help is a wise financial choice, not a sign of weakness.

“Recognizing you need help is the first step towards financial freedom.”

Credit counselling services provide advice made just for you. They help you understand your options and make a plan to beat your debt. Taking action now can prevent bigger financial problems later.

The Role of Credit Counselling in Debt Management

Credit counselling is key for Canadians to manage their debt well. It offers expert advice on planning your finances and budgeting. This helps you take charge of your money.

Professional Credit Counsellor Qualifications

Credit counsellors in Canada get thorough training to help with your money worries. They have certifications from trusted places and know a lot about managing your finances.

| Qualification | Description |

|---|---|

| Accredited Financial Counsellor Canada | Comprehensive training in financial counselling and debt management |

| Certified Credit Counsellor | Specialized education in credit and debt solutions |

| Financial Health Professional | Expertise in overall financial wellness and planning |

Initial Assessment Process

Your first meeting with a credit counsellor is a detailed look at your finances. They’ll ask about your income, spending, and debts. This helps them understand your financial situation.

Creating Your Financial Strategy

After assessing your finances, your counsellor will create a plan just for you. This strategy includes budgeting and long-term financial planning. It’s designed to help you reach your financial goals and stay financially stable.

“Credit counselling is not just about managing debt; it’s about empowering you with the knowledge and tools to build a secure financial future.”

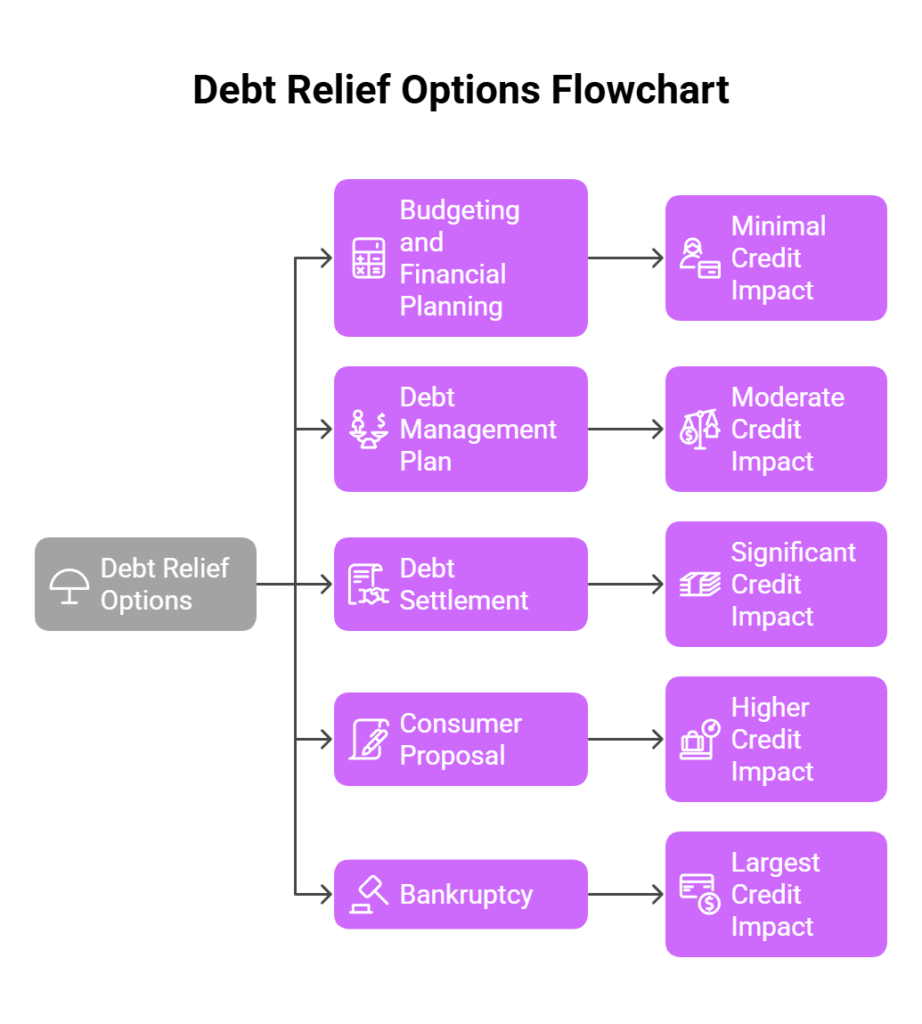

Comparing Debt Management Plan with Other Solutions

When you’re struggling with debt, you have many ways to deal with it. A Debt Management Plan (DMP) is a good option. But, it’s key to know how it stacks up against other choices.

Debt settlement means talking to creditors to pay less than what you owe. This can give quick relief but might lower your credit score. On the other hand, a DMP aims for full debt repayment, often with lower interest rates.

Bankruptcy is a last choice for those with too much debt. It can give a new start but affects your credit and finances for a long time. A DMP is a better choice, helping you pay off debts without the big credit hit.

| Solution | Debt Repayment | Credit Impact | Timeline |

|---|---|---|---|

| Debt Management Plan | Full repayment | Minimal negative impact | 3-5 years |

| Debt Settlement | Partial repayment | Significant negative impact | 1-3 years |

| Consumer Proposal | Partial repayment | Significant negative impact | 3 years after completion |

| Bankruptcy | Debt discharge | Severe negative impact | 6-7 years on credit report |

A DMP finds a middle ground between paying off debt and protecting your credit. It lets you clear your debts fully while possibly lowering interest rates and combining payments. This method helps you get back on track financially without the harsh steps of bankruptcy or the credit harm of debt settlement.

Steps to Enroll in a Debt Management Plan

Starting a debt management plan is a big step towards getting your finances back on track. It involves several important steps. Each step is designed to help you take control of your money.

Required Documentation

To begin your debt management plan, you’ll need some important documents:

- Recent pay stubs or income statements

- List of all debts and creditors

- Monthly expense breakdown

- Bank statements from the past three months

- Tax returns from the previous year

Meeting with Credit Counsellors

In your credit counselling session, you’ll have a detailed talk about your finances. Your counsellor will look at your income, expenses, and debts. They’ll create a plan just for you.

They’ll explain how a debt management plan works. They’ll also answer any questions you have about the process.

Negotiating with Creditors

After you agree to a debt management plan, your counsellor will contact your creditors. They’ll try to get better terms for you. This might include:

- Lower interest rates

- Waived late fees

- Extended repayment timelines

Your counsellor will keep you informed about the negotiations. They’ll help finalize your debt management plan. With their help, you’re on your way to a more stable financial future.

Impact on Your Credit Score and Report

When you join a debt management plan, it’s key to know how it changes your credit score and report. A DMP can help fix your credit, but its effects change over time.

Short-term Credit Effects

At first, your credit score might drop a bit. This is because:

- Your creditors may close some accounts

- Your credit utilization ratio might change

- The DMP notation appears on your credit report

Don’t fret – these changes are usually short-lived and part of the debt management journey.

Long-term Credit Recovery

As you move forward in your debt management plan, you’ll notice good changes:

- Regular, on-time payments boost your payment history

- Your debt-to-income ratio goes down

- Accounts are marked as “paid as agreed” once settled

These improvements help your credit score grow. Many Canadians see their scores rise and even go above their pre-DMP levels after finishing the plan.

Keep in mind, a debt management plan is reported differently than other debt relief methods. It shows you’re actively working to pay off your debts. This can be seen more positively by lenders in the future.

Monthly Payments and Program Duration

Joining a Debt Management Plan (DMP) means you’re making a big commitment. Your monthly payments are set based on how much you owe, how much you make, and what you need to live. This way, you can pay off your debt without sacrificing your quality of life.

A DMP usually lasts 3 to 5 years in Canada. But, it can be shorter or longer depending on several things. These include how much you owe, your income, and the deals you make with creditors. Paying on time is essential to reach your financial goals.

| Factor | Impact on DMP Duration |

|---|---|

| Total Debt Amount | Higher debt may extend the program |

| Income Level | Higher income can shorten repayment time |

| Creditor Terms | Favorable terms may reduce program length |

Life can throw curveballs that affect your DMP. Losing your job or facing medical bills might mean you need to change your payment plan. Working with your credit counselor helps keep your plan flexible and in line with your finances.

- Regular payments maintain program momentum

- Missed payments can extend program duration

- Financial changes may prompt plan adjustments

By sticking to your DMP, you’re making a big step towards financial security. Remember, every payment brings you closer to being debt-free. It also helps you get better at managing your money.

Working with Creditors Through Your DMP

A debt management plan helps you take back control of your money. It involves working with creditors to make payments easier. This teamwork benefits both you and your creditors.

Interest Rate Reductions

Credit counsellors talk to creditors to lower your interest rates. This can cut down what you owe a lot. Many creditors will reduce rates by 50% or more, helping you pay off debt faster.

Payment Consolidation Benefits

A big plus of a debt management plan is simplifying payments. You make one monthly payment to your credit counselling agency. They then split it among your creditors, making things easier for you and reducing stress.

Creditor Communication Protocols

When you have a debt management plan, how you talk to creditors changes. Your credit counselling agency becomes the main contact. This means:

- Fewer collection calls to you

- Regular updates on your progress

- Professional handling of any issues that arise

This makes talking to creditors easier and less stressful. It lets you focus on paying off your debt without worrying about creditor calls.

Life After Completing Your DMP

Finishing your Debt Management Plan is a big win. It’s a chance to start fresh and gain financial freedom. Let’s look at how you can use this success to build a stable future.

Building Financial Stability

After your DMP, planning your finances is key. Start by saving for emergencies. Set goals like saving for a home or retirement. Keep using your budgeting skills to track your money.

- Review your budget monthly

- Automate savings to reach your goals faster

- Invest in yourself through education or skills training

Maintaining Debt-Free Status

Staying debt-free needs careful choices and smart money habits. Avoid debt by living within your means and using credit wisely. Always think before buying big things.

Improving your credit score is vital. Try a secured credit card or be an authorized user. Always pay on time and keep your credit use low.

“The habit of saving is itself an education; it fosters every virtue, teaches self-denial, cultivates the sense of order, trains to forethought, and so broadens the mind.” – T.T. Munger

Financial planning never stops. Regular meetings with a financial advisor are helpful. They keep you on track and adjust plans as needed. Good budgeting and smart choices lead to long-term success.

Common Mistakes to Avoid During Debt Management

Managing debt can be challenging. Many Canadians face obstacles on their way to financial freedom. Let’s look at some common mistakes to avoid.

One big mistake is taking on new debt. While on a Debt Management Plan (DMP), it’s best to avoid credit cards or loans. This can slow down your progress and make it take longer to pay off your debt.

Another common error is missing payments. It’s crucial to stick to your DMP schedule. Late or missed payments can damage the trust you’ve built with your creditors.

Keeping financial changes secret is also a mistake. If your income drops or expenses increase, tell your credit counsellor right away. They can adjust your plan to help you stay on track.

Thinking a DMP is a quick fix is also misguided. Debt relief takes time and effort. Stay committed to your financial planning goals for the long term.

| Mistake | Impact | Solution |

|---|---|---|

| New debt | Prolongs DMP | Avoid credit use |

| Missed payments | Creditor trust loss | Set reminders |

| Hiding changes | Plan ineffectiveness | Open communication |

| Quick fix mindset | Unrealistic expectations | Long-term commitment |

By avoiding these common mistakes, you can increase your chances of DMP success. Stay focused on your debt relief goals and seek guidance from your financial planner.

Conclusion

A debt management plan can be a lifeline for Canadians struggling with overwhelming debt. It offers a clear path to financial freedom. You can regain control of your finances by working with credit counsellors and negotiating with creditors.

By doing this, you can potentially reduce interest rates. You can also consolidate payments into a single, manageable sum. This makes it easier to manage your debt.

While a debt management plan isn’t for everyone, it’s worth considering if you’re facing mounting debts. The impact on your credit score may be temporary. But the long-term benefits of becoming debt-free can far outweigh this short-term setback.

Remember, the journey to financial stability might be challenging. But the outcome can lead to a brighter future. It’s a chance to start fresh and build a stable, debt-free life.

If you’re unsure whether a debt management plan is right for you, seek advice from accredited credit counselling agencies. These professionals can assess your unique situation. They can guide you towards the most suitable debt relief option.

With determination and the right support, you can overcome your financial hurdles. You can build a stable, debt-free life. It’s a chance to start fresh and move towards financial stability.

FAQ

What is a Debt Management Plan (DMP)?

A Debt Management Plan helps you manage and pay off many debts. You work with a credit counselling agency. They help you make one monthly payment, often at a lower interest rate.

How does a DMP affect my credit score?

At first, a DMP might lower your credit score a bit. This is because of account closures or changes in how much you owe. But, making regular payments can slowly improve your score over time.

How long does a typical DMP last in Canada?

In Canada, a DMP usually lasts 3 to 5 years. This depends on how much you owe, your income, and what your creditors agree to.

Can I include all types of debt in a DMP?

Most unsecured debts, like credit card balances and personal loans, can be in a DMP. But, you can’t include secured debts like mortgages or car loans, or government debts like student loans.

How do I know if I need a Debt Management Plan?

You might need a DMP if you’re always missing payments or using credit for basic needs. Feeling overwhelmed by debt or struggling to pay multiple debts is also a sign.

What’s the difference between a DMP and debt consolidation?

Both aim to make paying off debt easier. But, a DMP involves working with a credit agency to negotiate with creditors. Debt consolidation is getting a new loan to pay off old debts, which might not involve professional help.

Can I use credit cards while on a DMP?

Usually, you’ll need to close your credit card accounts when starting a DMP. This stops you from getting into more debt while you’re paying off what you already owe.

What happens if I miss a payment on my DMP?

If you miss a payment, tell your credit counselling agency right away. They can help adjust your plan or talk to creditors to avoid penalties or ending the plan.

Are there fees associated with a DMP?

Many non-profit credit counselling agencies in Canada offer DMPs with low fees. These fees are often part of your monthly payment. They should be explained clearly before you join the program.

How do I choose a reputable credit counselling agency for a DMP?

Look for agencies accredited by the Canadian Association of Credit Counselling Services (CACCS) or Credit Counselling Canada. Make sure they are non-profit, open about their fees, and offer financial education along with DMP services.