The mortgage landscape is layered with complexities, but one of the most fundamental concepts is the hierarchy of lien positions. Every mortgage or loan secured against a property has a designated ranking, which determines repayment priority in the event of default. Understanding the differences between first and second mortgage positions can empower homeowners to make strategic borrowing decisions while safeguarding their financial stability.

Understanding Mortgage Lien Positions

How Lien Priority is Determined

Why Borrowers Use Second Position Mortgages

Why Lenders Don’t Like Seconds

Understanding Mortgage Lien Positions

A mortgage lien is a legal claim against a property used as collateral for a loan. These liens are ranked based on priority, which affects how debts are repaid if the borrower defaults. The positioning of a lien is a critical factor in determining the risk profile of the mortgage, with the first position holding the strongest claim.

First Position Mortgage

A first-position mortgage is the primary loan secured against a property, typically obtained to purchase the home. Because it has the highest priority, it usually carries lower interest rates and more favourable terms than subordinate loans. Lenders prioritize these mortgages because, in the event of foreclosure, they are the first to be repaid.

Second Position Mortgage

A second mortgage is an additional loan taken out against a property that already has an existing mortgage. Since it holds a subordinate lien position, it carries higher risk and therefore demands higher interest rates. Common reasons for taking a second mortgage include debt consolidation, home renovations, and investment opportunities.

READ MORE: What is a Second Mortgage?

How Lien Priority is Determined

Lien priority follows a simple rule: “first in time, first in right.” This means the first loan registered against the property takes precedence over subsequent loans. However, exceptions can arise due to subordination agreements, which allow a second-position lender to maintain priority when a first mortgage is refinanced.

Types of Second Position Mortgages

- Home Equity Loans – Lump-sum loans secured against home equity.

- HELOCs – Revolving lines of credit that use home equity as collateral.

- Private Second Mortgages – Loans issued by alternative lenders, often at higher rates.

Why Borrowers Use Second Position Mortgages

Many homeowners utilize second mortgages to unlock equity for various financial needs, such as funding business ventures, paying off high-interest debt, or covering emergency expenses. These loans can be beneficial when managed wisely, but they also come with inherent risks.

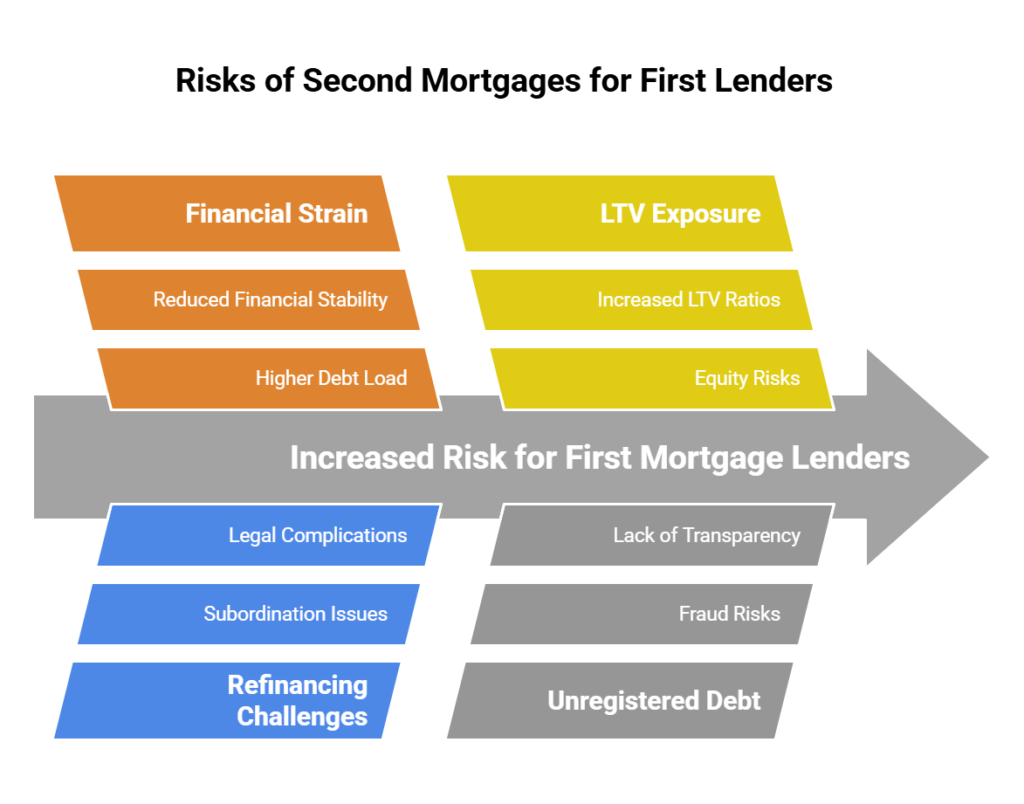

Why Lenders Don’t Like Seconds

A second mortgage is a loan that is secured against a property that already has an existing mortgage. It is considered “second” because it is subordinate to the first mortgage in terms of priority—meaning that if the homeowner defaults, the first mortgage lender gets paid first, and the second mortgage lender gets paid only after the first loan is settled.

Many lenders do not like or permit a second mortgage to be behind them. Lenders take on significant risk when offering mortgages and allowing a second mortgage behind their first mortgage can increase their exposure to potential losses. Many lenders do not allow second mortgages behind their first mortgage for the following reasons:

- Increased Risk in Case of Default

- Reduced Control Over the Borrower’s Financial Stability

- Complications in Refinancing and Subordination Issues

- Higher Loan-to-Value (LTV) Exposure

- Mortgage Insurers Prohibit It

- Potential for Increased Power of Sale

- Risk of Fraud and Unregistered Debt

- Lender-Specific Policies and Legal Clauses

READ MORE: Why Lenders Don’t Like Seconds

Subordination Agreement

A subordination agreement is a legal document that modifies the lien priority of two or more mortgages on a property. In the context of first and second position mortgages, this agreement allows a lender with a lower-ranking mortgage (such as a second mortgage or a home equity line of credit) to maintain or regain priority after changes are made to the first mortgage.

READ MORE: Understanding Subordination Agreements

Why is a Subordination Agreement Needed?

Typically, lien priority is determined by the order in which mortgages are registered on the property title. The first mortgage has priority, while any subsequent loans (such as a second mortgage) are subordinate. However, if a borrower refinances their first mortgage, the original mortgage is discharged, and the second mortgage would technically move into the first position.

Most lenders of refinanced mortgages require first position, which is where a subordination agreement comes into play. The second mortgage lender agrees to maintain its subordinate status, ensuring that the refinanced first mortgage regains priority.

Getting a Second Mortgage

If you have a first mortgage, can you just go out and get a second mortgage? The short answer is not always. While it is possible to obtain a second mortgage if you already have a first mortgage, several factors must align for you to qualify. You cannot simply go and get a second mortgage without ensuring that both your existing lender and a potential second mortgage lender allow it.

Ensure you answer the following questions:

- Does Your First Mortgage Lender Allow a Second Mortgage?

- Do You Have Enough Home Equity to Qualify?

- Do You Meet the Lender’s Qualification Requirements?

- Are You Choosing the Right Type of Second Mortgage?

- Can You Afford the Second Mortgage Payments?

READ MORE: Getting a Second Mortgage

READ MORE:

Understanding Subordination Agreements

Why Lenders Don’t Like Seconds

Summary

Navigating the mortgage landscape requires a clear understanding of lien positions, which determine repayment priority in case of default. A first-position mortgage is the primary loan secured against a property, offering lower interest rates due to its top priority in repayment. A second-position mortgage, on the other hand, is subordinate to the first, meaning it carries higher risk for lenders and typically comes with higher interest rates. Homeowners often take second mortgages to access equity for debt consolidation, renovations, or investment opportunities, but these loans require careful financial planning.

Lien priority generally follows the “first in time, first in right” rule, but subordination agreements can allow a second mortgage to remain subordinate when refinancing a first mortgage. Many lenders hesitate to allow second mortgages behind their loans due to increased default risk, refinancing complications, and potential fraud. Additionally, insured mortgages from CMHC, Sagen, and Canada Guaranty do not permit second mortgages.

Obtaining a second mortgage isn’t automatic—it depends on lender policies, available home equity, borrower creditworthiness, and affordability. Homeowners must ensure their first mortgage allows it, meet lender qualifications, and choose the right financing structure to avoid financial strain. Understanding these factors can help borrowers leverage home equity effectively while minimizing risk.