Archive

Article Archive

Ontario Variable Rate Mortgage Strategy

Reverse Mortgage: Independent Legal Advice (ILA)

Reverse Mortgages and the Affluent Retiree

Funding Your Retirement: Reverse Mortgage

Reverse Mortgage to a Second Dream Home

Reverse Mortgage: Cushion Against Inflation

Struggling Financially as a Senior

Key Features of a Consumer Proposal in Ontario

Mortgages: Consumer Proposal & Bankruptcy

Key Features of Bankruptcy in Ontario

Mortgage Availability in a Flood Zone

Who are Canada’s Private Lenders?

Who are Canada’s Mortgage Finance Corporations?

Canada’s Non-Federally Regulated Mortgage Providers

Who are Canada’s Mortgage Investment Corporations

Does the Stress Test Apply to Private Mortgages?

How Does the Stress Test Work?

American Financial Crisis in Canada?

What is Canada’s Mortgage Default Risk?

Why Canada Needed the Mortgage Stress Test?

What does the Stress Test Prevent?

5 Reasons to Escape the Rent Trap

Why Mortgages are Important to Canada’s Banks

Price of Commuting: Lost Time, Lost Life

Price of Commuting: The Daily Journey into Toronto

Is Ontario’s 407ETR The World’s Most Expensive Highway?

10 Ways Interest Rates Impact Housing Prices

10 Reasons Why Investment Demand Impacts Real Estate Prices

10 Ways Inflation Impacts Real Estate Prices

10 Ways Economic Conditions Impact Real Estate Prices

10 Reasons Real Estate is So Expensive

10 Ways Supply and Demand Impact Real Estate Prices

10 Ways ‘Location’ Impacts Real Estate Prices.

10 Ontario cities with Strong Property Value Appreciation

10 Fastest Growing Ontario Cities

Ontario’s Top Historical Cities

10 Factors Impacting Housing Supply

10 Shortest Ontario Commute Cities

Ontario’s 10 Most Affordable Cities

The Most Wanted Community Amenities

Ontario’s Top Lifestyle Cities

10 Variable Mortgage Strategies

How the Trigger Point Impacts Canadians

How to Take Advantage of Refinancing Opportunities

Difference between the Economy and Markets

Canadian Real Estate Lacks Capital

How to Control Inflation with Interest Rates

Interest Rates and the Canadian Dollar

How the Bank of Canada Steers the Economy

The Perfect Time for a Variable Rate Mortgage

How to Choose the Right Term Length for a Fixed Mortgage

What is Critical Illness Insurance

How to Make the Most of Prepayment Privileges for a Fixed Mortgage

Why Life Insurance is the Best Mortgage Insurance

How to Optimize Payment Frequency for a Fixed Mortgage

Record Wildfires Impact Lumber Pricing

How Alberta Leaving CPP Impacts You

Why Canadian Interest Rates Remain High

How Much is Airbnb Driving Up Rents

Experts Predict Canadian Dollar Fall

Re-Zoning to Create Affordable, Safe Neighbourhoods?

Why America Thrives and Canada Struggles

Small Business Debt: A Growing Concern for Canada’s Economy

The Housing Market and the Power of Lower Rates

Navigating Changing Interest Rates and Debt in Canada

The Importance of Private Sector Involvement in Affordable Housing

Investing in Real Estate and Infrastructure: Harnessing Long-Term Cash Flows

Defaulting on Your Mortgage? Exploring the Consequences and Solutions

Why a 3-Year-Fixed Mortgage May be a Bad Choice in 2024

Buy a property for $10 in Ontario: Town Makes Homeownership Affordable

Why Immigrants are Crucial for Canada’s Economy

Millennials Brace for Economic Pain

Toronto Real Estate: Dominance of Investors and Its Implications

Are You Prepared? Homeowners Brace for Mortgage Renewals

40-Year Canadian Mortgages: What you need to know.

London Addresses Homeless Crisis

The Impact of Mortgage Rates on Residential Property Values

Household Financial Stress Over High-Interest Rates

What’s So Special About 2% Inflation

How Much is Air BnB Driving Up Rent Prices?

Know the Dow, Build Your Down Payment

Mortgage Cash-Out Refinance in Ontario

Mortgage Refinance Options in Ontario

Mortgage Co-Signer: Risks & Responsibilities

Understanding Tenants in Common Ownership

Understanding Joint Tenancy Ownership

Why the First Time Home Buyer Incentive Program was Cancelled.

Navigating the CMHC Newcomers Program

Manulife One: Mortgage and Bank Account

Leverage Simcoe County Homeownership Program

Leveraging Peel’s BNI Homeownership Bridge Program

Leveraging GTA’s Habitat for Humanity

Leveraging the Kingston Homeownership Program

Leveraging the Dufferin Country Homeownership Program

Leveraging the Chatham/Kent Homeownership Program

Leveraging Gateway Muskoka Homeownership Program

Brantford’s B-Home Homeownership Program

Region of Waterloo Affordable Home Ownership Program

Leverage the Niagara Homeownership Program

Regional and Municipal Homeownership Programs

10 Big Benefits of Going Variable

Variable Mortgages. If you’ve ever surfed—or even watched someone surf—you know it’s all about balance. You don’t fight the wave; you ride it. That’s exactly what it feels like to hold a variable-rate mortgage. Sure, the water can get choppy, but if you’ve got good footing, it can take you further, faster, and often cheaper than the safer route.

Canadian Land Transfer Tax Calculator

Land Transfer Tax Calculator: Buying a home in Canada is a thrilling adventure — whether it’s a downtown condo, a family home in the suburbs, or a cabin near the lake. But between deposits, inspections, and closing paperwork, there’s one cost that often catches buyers off guard: the Land Transfer Tax (LTT).

Home Carrying Cost Calculators

… Understanding Carrying Costs: The Unsung Hero of Smart Homebuying When most people think about buying a home, they focus on one number—the price tag. But seasoned buyers, realtors, and mortgage professionals know that the real story lies beneath the surface. The...

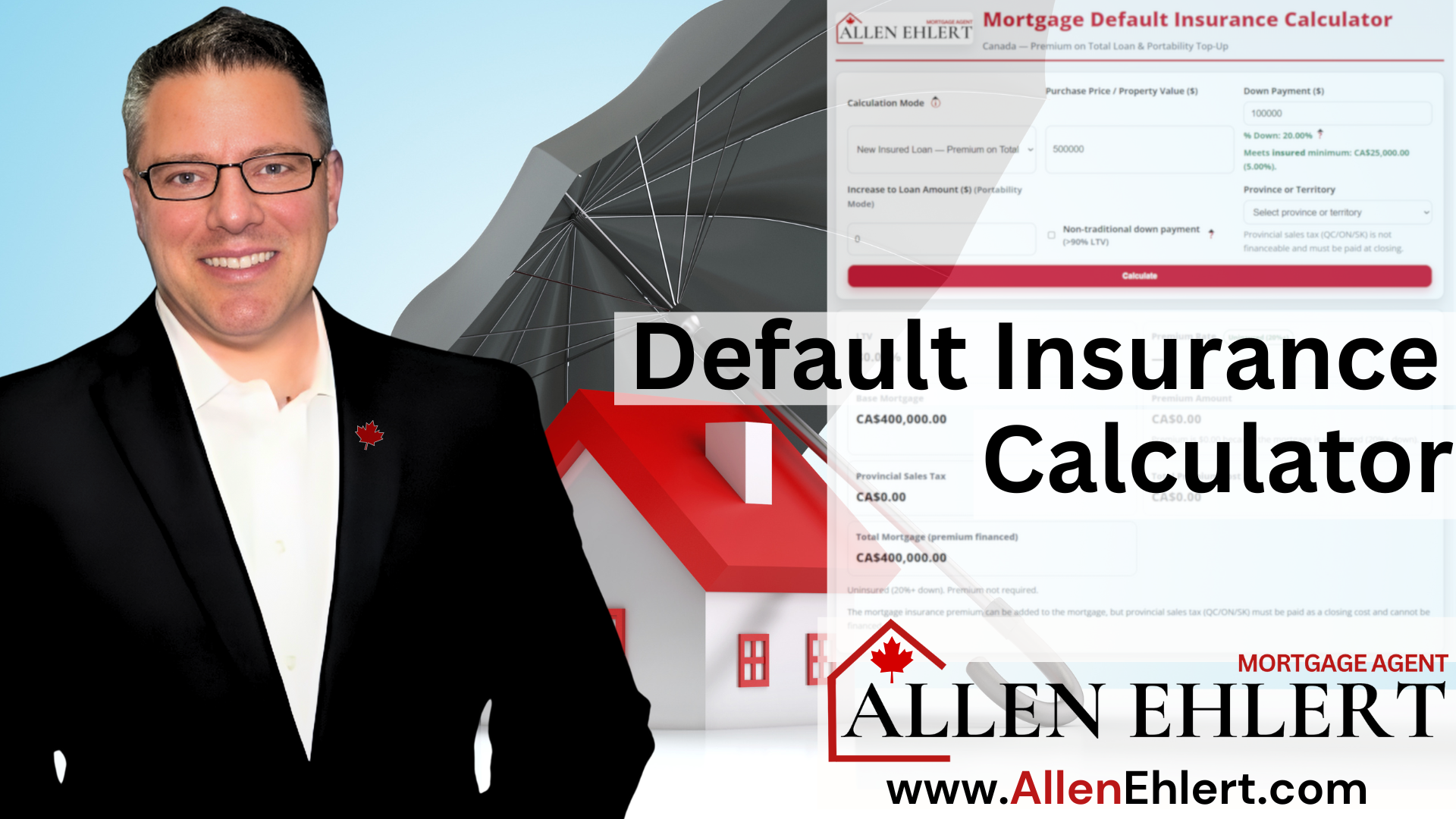

Mortgage Default Insurance Calculator

Mortgage Default Insurance Calculator: Buying a home in Canada can feel like stepping into a maze of numbers, acronyms, and fine print — but it doesn’t have to. Whether you’re a first-time buyer or a seasoned investor, understanding how default insurance works is key to knowing your real costs and options.

Canadian Closing Costs Calculator

Canadian Closing Costs Calculator: Buying a home is one of those life-changing moments that’s equal parts thrilling and nerve-wracking. Between scrolling listings, making offers, and imagining your first morning coffee in the new kitchen, it’s easy to overlook one key detail — closing costs. These aren’t the fun, HGTV-type parts of buying a home, but they’re essential.

The Networking Myth

The Networking Myth: As a mortgage agent working alongside realtors, accountants, and financial planners, I see this disconnect every day. Talented professionals doing everything “right,” yet wondering why referrals feel harder to come by. The issue isn’t effort or skill. It’s that the rules of social engagement—and therefore business growth—have changed.

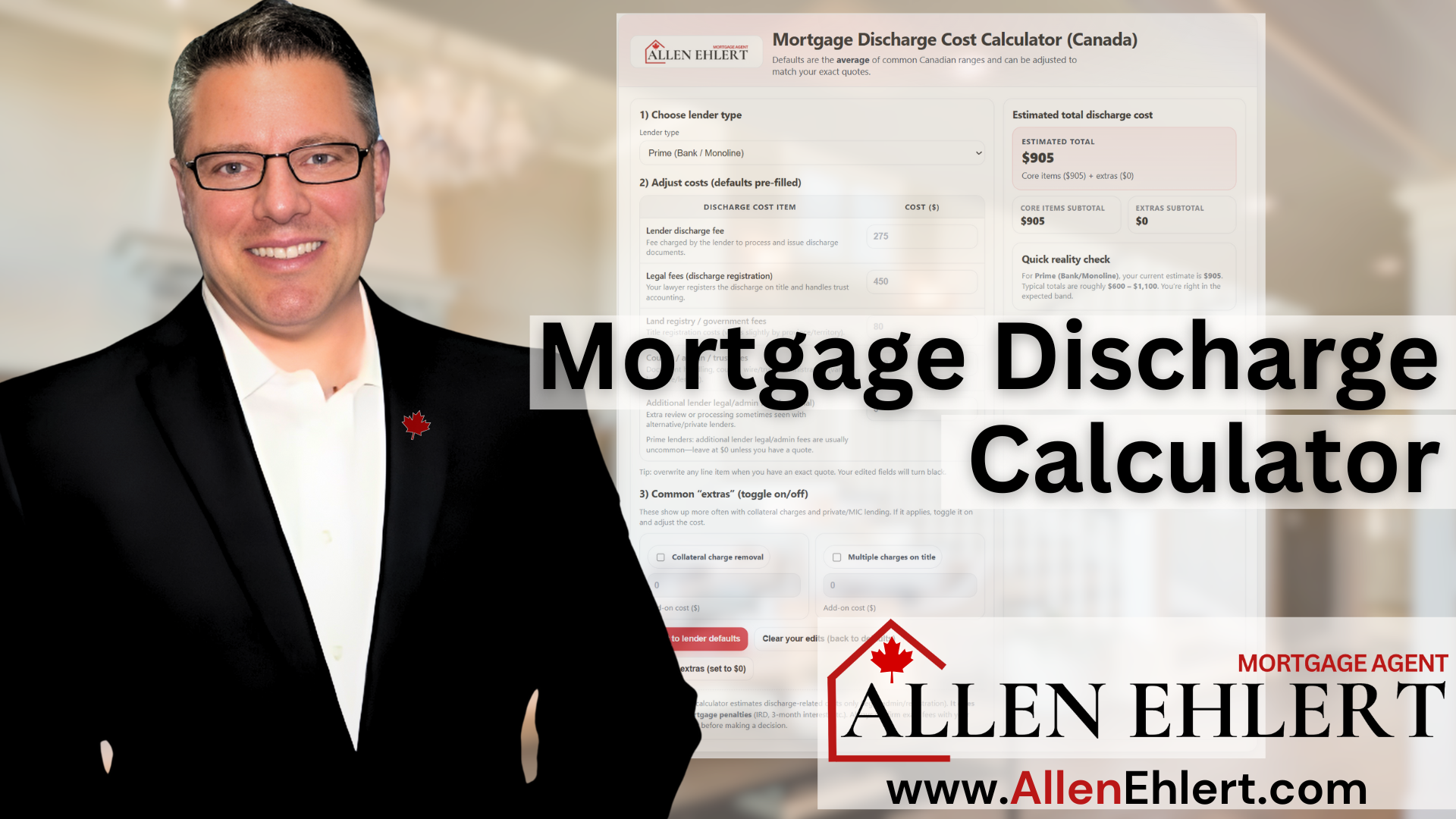

How to Use My Mortgage Discharge Cost Calculator

Mortgage Discharge Calculator: This tool is designed to help you see—clearly and early—what it actually costs to remove a mortgage from title, based on the type of lender you’re dealing with. Whether you’re refinancing, switching lenders, selling a property, or restructuring debt, knowing these numbers in advance puts you back in control.

Non Resident Tax Rebates (NRST, NRPDTT, BC PNP, etc.)

Foreign Buyer Tax Rebates (NRST, NRPDTT, BC PNP): When you first arrive in Canada, buying a home feels like crossing the finish line of a marathon—only to realize there’s another race waiting at the starting line: understanding the taxes, rebates, and programs that affect newcomers. One of the biggest hurdles foreign buyers face in Ontario is the Non-Resident Speculation Tax (NRST)—a hefty 25% charge on residential property purchases by non-residents.

Why My Pre-Approval Is Better

Pre Approval: When you’re getting ready to buy a home, that pre-approval letter feels like a badge of honour — proof that you’re serious, qualified, and ready to make your move. But here’s what most buyers (and most realtors) don’t realize: not all pre-approvals are created equal.

Why You Need a Mortgage Agent

Mortgage Agent. Buying a home isn’t just a purchase—it’s a leap into the next chapter of your life. And with rates swinging, rules tightening, and mortgage options multiplying faster than smartphone models, you deserve someone who’s dedicated to you and no one else. That’s where a mortgage agent steps in—your advocate, your strategist, your buffer against costly mistakes.

Stop Scrolling Realtor.ca

Get a Mortgage Agent first: Most people start their homebuying adventure exactly backwards. They hop onto Realtor.ca, fall in love with a gorgeous kitchen, picture their dog in the backyard, and then—usually with a little dread—they think, “Okay… how do we actually pay for this and what can we afford?”

Need a Mortgage? Start Here.

Need a Mortgage? Start Here: Buying a home—especially your first—can feel like stepping into a world where everyone else seems to have the rulebook but you. Rates, lenders, documents, jargon… it’s enough to make anyone feel like they’re drinking from a firehose. But when you follow the right steps in the right order, everything becomes clearer, calmer, and surprisingly empowering.

Protect Your Mortgage

Mortgage Protection Insurance: Buying a home, especially your first home is one of those big, life-defining moments. You and your partner have been budgeting, working with your mortgage agent, hunting down listings, talking to realtors, and imagining what that first night in a place that’s finally yours will feel like. But beneath all the excitement, there’s a quieter, more grown-up question that every couple needs to ask—“If something unexpected happens, can we not lose this home we worked so hard for?”

Understanding Contributory Income

Contributory Income: Every once in a while, a mortgage file comes along that makes you smile—not because it’s easy, but because you know exactly what lever to pull to make the deal work. Contributory income is one of those levers. It’s the quiet, seldom-talked-about income source that can turn a “maybe” into a confident “yes,” especially when buyers are stretched, ratios are tight, or affordability feels like a moving target. And if you’re a realtor guiding clients or a borrower trying to qualify, understanding how contributory income works is like unlocking a hidden chapter in the rulebook.

Understanding Shelter Costs

Shelter Costs: If you’ve ever felt like lenders were speaking a different language when they talk about “shelter costs,” you’re not alone. Clients often look at me like I’m explaining astrophysics when I break down why lenders assign a shelter cost—even when a borrower is living in their parents’ basement and paying nothing more than a smile and a promise to take out the garbage.

10 Ways Urbanization Impacts Real Estate Prices

Urbanization trends significantly impact real estate prices due to a variety of interconnected factors: Increased Demand in Urban Areas Limited Supply in Dense Areas Changing Lifestyles and Preferences Infrastructure and Amenities Economic Opportunities Investment...

Featured Publications

Articles

- Extended Amortizations and Hypothetical Calculations

Office of the Superintendent of Financial Institutions (OSFI) - Minimum Qualifying Rate for Uninsured Mortgages

Office of the Superintendent of Financial Institutions (OSFI) - Residential Mortgage Underwriting Practices and Procedures

Office of the Superintendent of Financial Institutions (OSFI) - Guideline on Existing Consumer Mortgage Loans in Exceptional Circumstances Financial Consumer Agency of Canada

Book: “The Program”

- Part 1 – Building Your Down Payment

- Part 2 – Mortgage Payoff Strategies

- Part 3 – Building Wealth Through Real Estate

Get a free subscription to “The Mortgage Insider” containing rate updates and financial strategies!